The Infinite Banking Concept

The infinite banking concept can be a highly efficient way to manage your finances and create a bank for yourself. It involves using an insurance policy as a tax-free financial vehicle, which can then be leveraged for investments, emergencies, and even retirement. This concept has been around since the 1950s but has only recently gained traction in famous financial circles and social media. In fact, Walt Disney used life insurance to finance the build for Disneyland. In this article, we will dive deep into the infinite banking concept and explore how you can use it to your advantage. Learn more about its advantages, some things to avoid and how you can start using this concept to become financially independent while creating generational wealth.

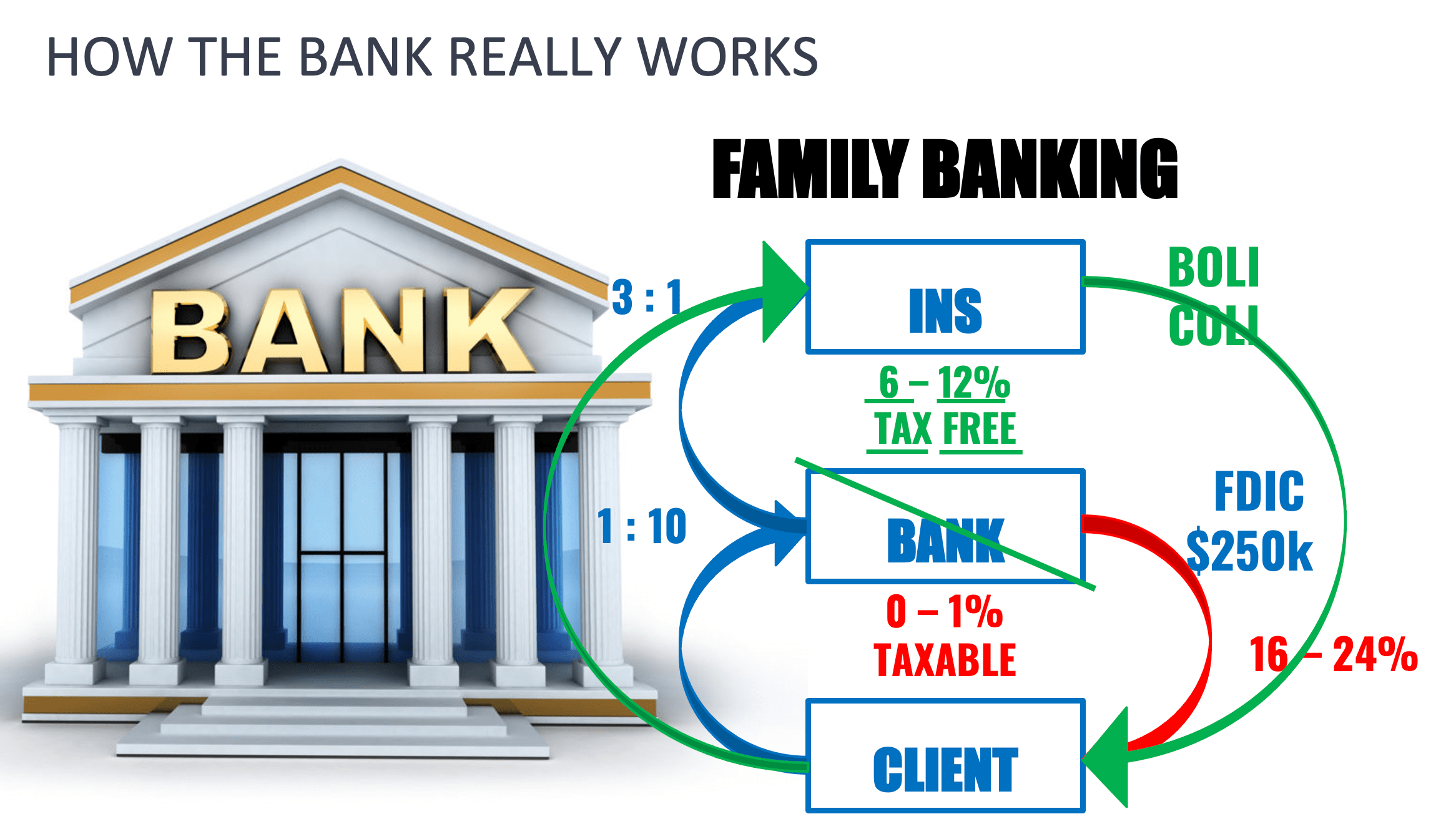

What Is the Infinite Banking Concept?

The infinite banking concept is a financial strategy that allows you to use your life insurance policy as your bank. It is like building a home from scratch; first, you must find a reliable and quality contractor to build the home properly and structure it how you want it to look. There will be upfront costs like land, architect, permits, materials etc. Over the years, the home builds equity which you can borrow from at any time using a HELOC. When the loans are paid back, you then have that equity to borrow again later, but while you have loaned out, your equity never stops growing. Adding additions or upgrading the home continues only to add more equity.

With a life insurance policy, you need to find a good agent who understands your financial goals and will structure the policy correctly. Most of the insurance cost is incurred in the first couple of years (the land, the architect, surveying, etc.) The equity in your house is the cash value, and it continues to grow each year. Unlike a home, your cash value is guaranteed never to lose equity. Each year you can remodel or add additions to your home (premium), which only increases your home's equity, the cash value. The cost of adding those extras costs you less and less each year because the main structure of your home (the cost of insurance) has already been incurred. Like a HELOC, you can borrow from the cash value while allowing your home's equity to grow continually. The interest on these loans is typically between 4% and 5%.

"Every businessman should be in two businesses – the one in which he earns his living – and the banking business that finances what he does for a living. Of the two, banking is the most important" - Nelson Nash.

Nelson Nash first introduced this concept in his book, Becoming Your Banker. The idea is to create your banking system so that you and your family are not reliant on banks or other financial institutions. But at the same time, have your cash value working for you for the remainder of your life. For example, you can use your life insurance policy to fund major purchases, such as a car, finance a business startup, a child's college tuition, etc., by borrowing against the policy's cash value. You can take out as many loans as you want and get to set the terms of repayment.

One of the main advantages of using the infinite banking concept is that it allows you to keep your money within your control. As a result, you are not at the mercy of banks or other financial institutions when borrowing and paying back your cash.

If you're looking for a way to finance all your purchases while creating generational wealth, the infinite banking concept may be right for you. All you need to do is change where your money goes first. Your money goes into your "house" or life insurance policy first. Then, year after year, you add additions to your home, so your equity continues to grow and compound yearly tax-free.

How Much Money Is Needed for Infinite Banking?

To have an infinite banking system, one needs to just start, the sooner you can begin in life, the more time you allow the policy to grow; that is the power of compounding. Going back to the home analogy, if you were to build a home for a child, their home would have more years to build equity. It is better to start with less money than never to start at all. Time is the only ingredient that can't be made up for. Every month and year that passes is time that your money could have been in motion and working for you.

When building your financial house, or your bank, your premium should be mindful but meaningful. It should be doable but significant to achieve your financial goals on your timeline. For example, if your goal is to put 30k down for a real estate investment in two years, the policy will need to be structured correctly, so your "home" has enough equity two years later to borrow the 30k for the investment.

The bottom line is that no set amount of money is needed to create an infinite banking system. It depends on what one's goals are, the timeline for achieving those goals and how much money one needs available.

How Infinite Banking Works

With IBC, you take out a cash-value life insurance policy that is properly structured, which means minimum death benefit and maximum cash value. It can only be done with a whole life policy. But you can become your own bank using an IUL. This is because whole life has guaranteed dividends and IUL's do not. You are not getting a life insurance policy for the death benefit. You are getting a bank that is safe, protects your wealth, gives you liquidity options, and allows your money to grow tax-free. The living benefits give you access to the death benefit in case you develop any critical or chronic illness. The death benefit passes wealth to your heirs' tax-free.

Advantages of Infinite Banking

There are many advantages of infinite banking, but here are my top three:

1. You are in control of your money.

When you have your bank, you have liquidity. This means you control your money and can decide when and how it is used. That can be real estate investments, home improvements, vacations, college tuition, or starting a business. You are not at the mercy of a bank or other financial institution begging for a loan; you set the terms.

2. Your money is always working.

When your money goes into your bank first, it never stops working for you. It will only continue to compound tax-free. But, once it goes into the policy, that money is in motion for good.

3. It's Safe.

Your life insurance policy is not an asset; it is insurance. Therefore, your cash value is protected from taxes, creditors, predators, the IRS, market losses, etc.

Disadvantages of Infinite Banking

Potential policyholders should be aware of some disadvantages of infinite banking before getting a policy. Firstly, there are costs to having insurance, but those costs come down year after year. If set up correctly and appropriately funded for the first 5 to 7 years, the money earned in the policy covers the cost of insurance. The policy becomes self-insured. Secondly, it needs to be treated like an actual bank. Loans and interest should always be paid back to your bank.

Finally, it takes discipline from the policy owner. The policy only works if they are willing to be patient and play the long game. It is not something you start if you are going to quit after two years. It takes 4 to 5 years to have a successful bank.

"Play long-term games with long-term people. All returns, whether in wealth, relationships, or knowledge, come from compound interest."

- Naval Ravikant

Schedule a no-obligation consultation with me if you want to learn more about IUL's and how it might help you achieve your financial goals now and in the future.

*Disclosures: Educational purposes only. No statements should be considered advice. Past performance and numbers do not guarantee future results. Life insurance is not an investment.

"When the government creates a problem and gives you a break, it benefits them more than you. In the case of taxation, they could help consumers by cutting taxes; instead, they offer “tax breaks” such as retirement and pension plans"

- Nelson Nash

© 2023 LiveLegendarylife.net | All Rights Reserved